Axell Hub conducted various interviews with its network of insurance executives over the past weeks in order to analyze the current state within large insurance companies and deduce future scenarios for the development of the entire industry. Here is what we found:

The world declared a state of emergency and is quarantining its population. Due to strict gathering restrictions, stores are forced to close and employees work from home, where applicable. Although the necessity of a Digital Transformation is not a new trend, now we realize many organizations still lag behind and are fiercely impacted by the shutdown. Their internal processes and channels to the market were just not setup yet for this very scenario, which causes tremendous financial problems. However, some corporates, but even more digital startups, use the pandemic to demonstrate their resilience and show the impact of their digital excellence efforts from the past.

One thing is for sure: The crisis will accelerate fundamental shifts in our private and business life and the more we get used to the decentralized way of living, the faster the broad adoption of digital tools will increase in our society. Does this mean that COVID-19 is the tipping point for Digital Transformation?

Some insurance business lines suffer, some benefit

Many insurance companies wonder what impact the accumulation of a large number of claims within a fairly short time span means to their portfolio and if their survival is even at stake (in case COVID-19 is covered). This applies to business interruption insurances, health or life, and many more domains.

Other business lines, however, like non-life or general insurance might even benefit due to the crisis. For example, the decreased use of private vehicles leads to fewer accidents, which leads to higher profits. Interestingly enough to look at are the postponed events like the Tokyo Olympics, who have an estimated coverage of USD 2bn (KPMG). Given that insurers forward the majority of their risks to re-insurers, they might carry the biggest part of financial burdens. Additionally, many insurers seem to have learned their lessons from the SARS outbreak in 2003 and consequently excluded pandemics from their policy offerings.

The crisis could be a wake-up call for the industry

Furthermore, financial damage occurs if agents cannot visit their clients anymore. New clients can hardly be on-boarded through the traditional channels. Meanwhile, the production levels of agents decrease significantly as many cannot do their job from home as efficiently or are just not used to online collaboration tools, which are at the latest now about to be installed at every company.

But there is also light at the end of tunnel. The crisis might be a wake-up call to improve long-distance collaboration, increase the adoption of modern technology and gain visibility through online marketing as people spend more time on the web. Organizations that placed too much focus on their daily operations at the expense of investing in digital for long-term resilience must be woken-up now. The value of digital operations, products and channels has never been more obvious. Thus, many insurers approach IT-providers and FinTechs to work on quick-wins in order to keep their operations running.

Transformational boundaries seem identified, but not overcome yet

Insurance executives we surveyed, mostly see Digital Transformation as an ongoing endeavor to improve the customer journeys and make the overall interactions with the business easier, intuitive and more customer-friendly. For instance, while starting Netflix, the platform immediately knows where you interrupted your last movie. This is what is needed for incumbents in the insurance industry as well, one innovation leader said.

Many executives mentioned their problems with project work, task management and tracking, while others claim they got used to the situation quite quickly as they have already been equipped with tools to work from home. Group compliance is still considered as a main inhibitor to work with modern video-conferencing, project management, or cloud based file-management tools.

In one case a video consultation software was introduced for the agents, which even covered the possibility to complete the necessary paperwork and remote signature thorough an app. Unfortunately, when all agents started to use the system at the same time, it collapsed. The high demand was just too much for the IT-architecture, so all call client meetings got cancelled. But there are not only technological problems, in the majority of cases the user interface of the agents’ provided software is quite outdated in many ways. Redundant questions have to be asked during a consultation or while screen sharing with clients, agents are often embarrassed given the user-unfriendly design and structure of the forms.

Other insurers found many agents were not familiar with digital tools at all and consequently cannot interact with their clients, even if possible. To handle the poor adoption levels, intense trainings will be necessary. Furthermore, digital leadership is a new domain for most executives, who suddenly feel out of power as their traditional management habits cannot be continued remotely. In this regard, trainings are in demand too.

Data-enabled operational efficiency will be the premier focus

Warren Buffett once said: “When the tide goes out, you discover who’s been swimming naked.” In other words, now is the time when people realize if you really transformed as a company or if you just wrote nice marketing phrases. In any case, the current situation is likely to accelerate the serious transformation of the insurance industry. In future we might consider this moment as the ‘FinTech Moment’.

This means incumbents holistically begin to upgrade their businesses and implement first-class digital interaction capabilities. Self-service portals for agents and policyholders, responsive websites, apps for immediate policy service and claims as well as modern call center CRMs are very critical in order to achieve customer satisfaction. Operational efficiency has to be increased through the usage of collaborative tools and processes have to be automated with RPA or AI to reduce manual labor and errors. Many more operational arenas can be transformed, such as data-driven ratings that augment the assessment of risks.

New product and channel innovation will deliver added customer-value

While becoming more and more digital, cyber-risk and data security play vital parts in order to defend attacks from the outside. It is crucial for insurance companies themselves; but also for their customers, as they will increasingly look for cyber-insurance products, given the crisis also forces them to innovate. Cloud computing is another topic, where insurers lag behind. With an increasing number of people working remotely, systems have to offer more bandwidth and capacity than available on-premise. Once operations are cloud-based, new job models and access to different talents are possible as companies could look to hire independently of location.

These operational examples have to be priorities, alongside channel and product innovation. People will demand around-the-clock availability across human and virtual channels as well as an holistic brand experience in an omni-channel way, which means data is shared instantly across all channels. Also, products will have to become more personal and smarter at the same time. Particularly during the current crisis, people might be frustrated about their constant car insurance payments, despite presenting much less risks, given the fact most people are staying at home and use the car for grocery shopping only. As a consequence, policies could be on a pay-as-you-drive basis and differ based on individual risk levels and distance driven.

The negative impact will especially hurt the early-stage startup ecosystem

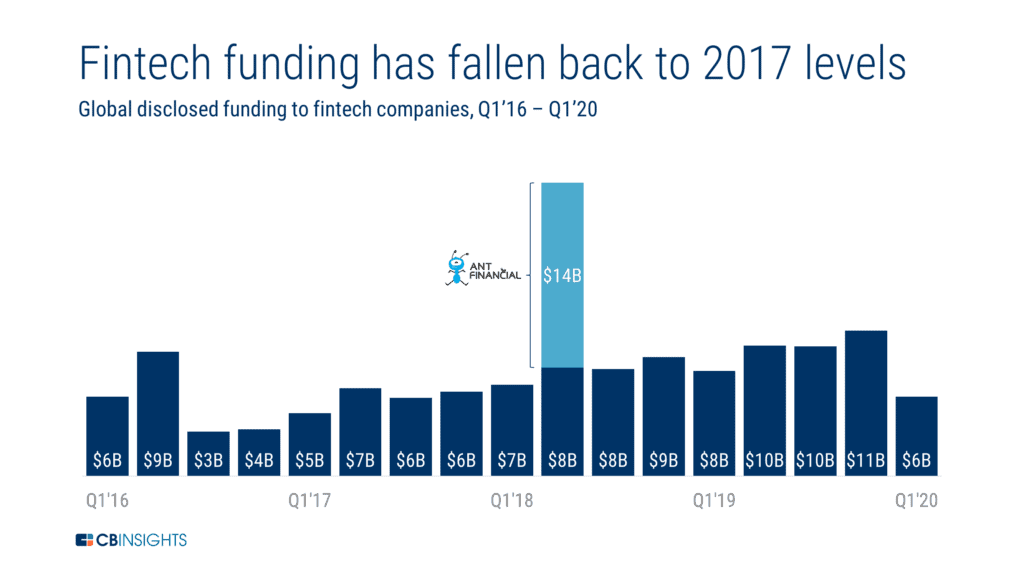

What might be new for the incumbent world, is already status quo in the InsurTech or FinTech world. FinTechs offer a variety of data-driven products or digital process-enabling tools for traditional companies. This is also why one must differentiate between challengers and enabler startups. While many customers will turn to digital challenger startups and use their tech-products, enabling companies will find it hard for the foreseeable months to win new corporate pilot-clients. Considering COVID-19, the year 2020 seems to be a challenging one. Unless they have the necessary funding in place for the next 18 months, chances are low they find investors who want to take risks as the bar for funding raises during crisis times. Also, funding has reached the lowest level since 2017 and deals are falling across geographies.

For challengers, the bad IT-infrastructure of incumbents and the subsequent poor customer experience will usher many clients in their direction. Challengers will be the winners of the crisis, which most likely leads to very active M&A activities in the years to come – similar to the post-GFC following 2008. With the consolidation of the market, insurance companies will have acquired their digital vehicles. To foster transformation, incumbents will run a group of two speeds, but sooner than later try to get rid of their legacy IT and utilize their new tech-vehicle as their premier product to all clients. Either the new tech is brought to their traditional clients or vice versa.

Partnering up with FinTech-enablers is the quickest way to build technological solutions

While this is a possible way to gain digital capabilities as an incumbent, integration often leads to additional obstacles and expenses. Alternatively, partnering up with enabler startups from the early stages and co-designing tailored solutions, might be a better, more cost effective way to foster cultural transformation and build up structures that fit to the corporate mother. However, conducing a pilot project with startups is not an easy undertaking though. It requires a clear goal, executive support and budget as well as precise governance and responsibilities. In order to bridge cultural boundaries, a facilitating party, who is experienced in both the startup and the corporate world is a necessary ingredient for project success. Different expectations regarding working speed, politics and contracts cause project to fail if not facilitated sensibly. Done right, startups can be the engine for digital transformation. Done right, they can enable the ‘FinTech Moment’.

To summarize: Corona doesn’t kill sales, bad IT and a bad customer experience do. Insurance companies need to start working on new customer-centric business models, all enabled by data-driven technologies. The collaboration with the right startups can lead to quick-wins in the short term and entirely new business streams in the mid-term. Axell Hub, being located in the heart of the Startup Nation in Tel Aviv, works closely with local ecosystem of 500+ FinTech startups and helps insurance and asset management companies regain their old strength – but now, in the digital world.